Falling crude prices raise questions over US oil production

Diamondback has warned of declining activity, but not every producer agrees

8 minute read

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed examines the forces shaping the energy industry globally.

Latest articles by Ed

-

Opinion

US Congress threatens to cut support for nuclear power

-

Opinion

It’s looking bleak for clean energy in the US as Congress threatens to shred the Inflation Reduction Act

-

Opinion

Can we add dozens of giant new data centres to the electricity grid?

-

Opinion

Falling crude prices raise questions over US oil production

-

Opinion

Tariffs begin to redirect global energy trade flows

-

Opinion

Energy Gang and Interchange Recharged join forces to discuss flexibility on the power grid

President Donald Trump was elected in part because of voters’ concerns about rising prices. Reducing the cost of living has been one of his declared objectives. His record so far has been mixed: consumer prices excluding food and energy continue to rise, albeit at a much slower rate than at the peak of US inflation in 2022.

One product that has come down in price is gasoline. The average US retail price of regular gasoline was US$3.147 per gallon this week, down almost 50 cents a gallon from its level a year ago.

But while the fall in fuel prices has been very welcome for American consumers, it is a double-edged sword. Falling oil prices, taking US crude to about US$60 a barrel as of Friday morning, have raised concerns about the outlook for the US industry.

Those concerns were underlined this week by a letter to investors from Travis Stice, chief executive of Diamondback Energy, a leading oil producer in the Permian basin. The US shale industry has reached maturity, he wrote, and the tailwinds provided by improvements in technology and operational efficiencies are now being outweighed by those from more challenging geology.

“We believe we are at a tipping point for US oil production at current commodity prices,” Stice went on. “As crude pricing moves lower for a period of time, as it has over the last month, we expect activity to slow and oil production to decline.”

Reflecting that view, Diamondback is cutting its planned capital spending this year by about US$400 million, or 10%, and scaling back its drilling programme.

“We are taking our foot off the accelerator as we approach a red light,” Stice said.

Those decisions highlight a central tension in the administration’s energy strategy. It wants to see lower fuel prices for consumers, but also stronger oil and gas production. Reconciling the two is not easy.

President Trump often cites gasoline prices as evidence that his economic strategy is working. “Gasoline is down at numbers that nobody believes possible,” he told an interviewer on NBC News last weekend. “You know why they’re down, by the way? Drill, baby, drill. We’re drilling like crazy right now.”

But that explanation for the price movement is not really accurate. At the start of the year, 589 rigs were drilling for oil and gas in the US, according to Baker Hughes. Last week, that number was slightly lower, at 584. There is no evidence of a renewed drilling boom in the US.

Worries over the outlook for global economic growth and the decision by some OPEC+ countries to step up production increases have had a more significant influence on crude prices.

Diamondback’s comments raise the prospect that those factors could lead to a sharper slowdown in activity in the shale industry and a decline in US oil production.

The Wood Mackenzie view

Diamondback is a widely admired company with a strong track record. But its views on the outlook for the industry are not necessarily shared by all its competitors and peers, Wood Mackenzie analysts say.

ExxonMobil and Chevron, both large operators in the Permian basin, also made comments about the outlook recently as they released first quarter earnings. They sounded generally more positive.

Chevron said in its investor call that it expected growth in the Permian to resume in the second quarter, with increased hydraulic fracturing activity. Mike Wirth, chief executive, said the company was “very pleased with performance in the Permian and feel very good about the outlook for this year”.

He added that Chevron had good visibility on activity across the region, because it had an interest in one in five wells there, and “we don't really see any actions that have been taken to pull back by our partners.”.

In its investor call, ExxonMobil did not discuss the Permian in any detail, but said it was driving down costs and increasing efficiency to bring its breakeven oil prices to US$35 a barrel by 2027, and US$30 a barrel by 2030.

ConocoPhillips, which reported earnings this week, similarly indicated it would not be rushing to cut activity. It has reduced its planned capital spending for 2025 by about US$450 million, but that is being driven by capital efficiency and optimisation. It does not reflect any material change to activity in the US Lower 48 states, and the company’s guidance for production this year remains unchanged.

Ryan Lance, chief executive, said: “You shouldn’t expect a lot of things to change out of our company at these kinds of prices… For us, it’s: Don’t whipsaw this thing too hard right now, and use some of the strengths we have as a company.”

Companies are taking differing views depending on their specific circumstances, including their asset bases, their operational efficiency and their balance sheets. The net effect on Lower 48 oil production looks likely to be slow growth this year and a slight decline in 2026, on Wood Mackenzie’s latest forecasts.

Before our latest forecast revision, Lower 48 oil production was on track to grow by approximately 250,000 b/d in 2026, says Nathan Nemeth, Wood Mackenzie’s principal research analyst for Lower 48 Upstream. Taking the economic impact of the latest tariff announcements into account, we have cut out our oil rig count forecast by 10%, and the 2026 production outlook has shifted to a decline of 40,000 b/d.

That projection of a broadly flat outlook for Lower 48 oil production is an important corrective to some of the excitable headlines that have been circulating about “peak shale”. In fact, a slowdown in activity now might actually help push back the peak (which is more accurately described as a plateau).

Wood Mackenzie has for a while been projecting that as the best drilling locations get used up, US oil production will reach a plateau and stop growing around 2029. Less drilling now could mean that the inventory of high-quality locations lasts for longer.

However, these forecasts are based on the current oil price outlook, with West Texas Intermediate (WTI) crude currently at around US$60 a barrel.

If the economic situation deteriorates and the oil price outlook continues to weaken – with WTI dropping to US$50 a barrel or lower – then the outlook for activity and production could look significantly worse.

ConocoPhillips’ Lance gave an indication of that this week, when he talked about how the company was keeping planned activity in the Lower 48 unchanged.

“Would we have to look at potentially doing something different at $50?” he said. “Sure, we would. But that’s not our view today, and doesn’t represent where we think the market is going to be for the next few years.”

In brief

Pedro Sánchez, prime minister of Spain, has insisted he will not deviate “a single millimetre” from his commitment to renewables, despite the blackout that left the country without power for many hours last week.

Wood Mackenzie analysts identified three factors that contributed to the vulnerability of the electricity system: high renewable penetration, reduced conventional capacity and limited interconnection between the Iberian peninsula and France. The official inquiries into the blackout could take three to six months.

The US and the UK have agreed the key features of a new trade deal, the first such agreement since President Trump’s announcement of steep tariff increases last month. The agreement leaves in place the recently introduced 10% tariff on US imports from the UK, but includes relief from higher tariffs on goods including vehicles, steel and aluminium.

In return, the US is getting a series of benefits in greater access to UK markets, creating a US$5 billion opportunity for new exports, the White House said. One of the most significant changes is for ethanol: US exports to the UK have faced a 19% tariff, and that is being cut to zero.

The agreement with the UK was expected to be one of the easier ones: it has been running a small deficit in its trade with the US. Negotiations with other economies that run large goods trade surpluses with the US are expected to be more difficult. The EU this week set out plans for more potential retaliatory tariffs on US products, including electrical equipment, bourbon whisky and Boeing airliners. The new tariffs could be applied if negotiations with the US over a new deal break down.

Other views

The coming geothermal age – Simon Flowers and others

Iberian blackout: let the finger pointing begin – Brian Gaylord and Peter Osbaldstone

Where next for metals markets in 2025? – Robin Griffin

How will the lithium market rebalance? – Allan Pedersen

Aluminium at a crossroads: synchronising supply growth with decarbonization – Shashank Sriram

What’s next for copper? – Emily Brugge

Cameron LNG maintenance highlights fragility in spring gas demand – Daniel Myers

E-methane: a promising low-carbon alternative to natural gas? – Danish Sunasra

Quote of the week

"I think Russia – with the price of oil right now, oil has gone down – we are in a good position to settle. They want to settle, Ukraine wants to settle."

President Trump suggested that the decline in the price of oil could help put pressure on Russia to agree to a peace deal over Ukraine.

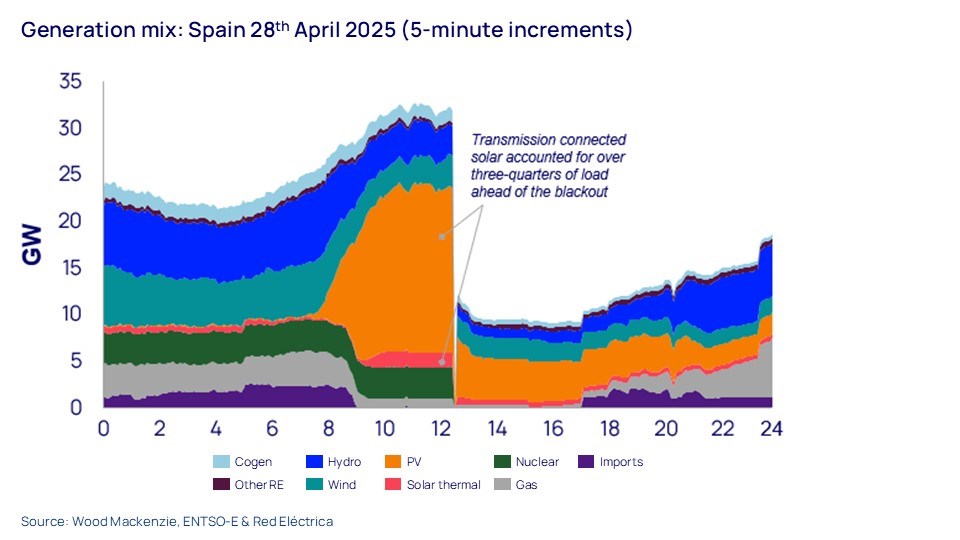

Chart of the week

This comes from the new report on last week’s blackout in the Iberian peninsula by Wood Mackenzie’s Brian Gaylord, a principal analyst, and Peter Osbaldstone, our research director for European power. The precise triggers that started the system failure are still unknown, and may not be for some time. Official investigations are underway. But Gaylord and Osbaldstone point to a range of factors that increased the vulnerability of the Iberian power grid, including its heavy reliance on solar generation at the time of the incident.

For more on what happened and why, download the free report. This is one of two reports we have produced relating to the blackout, with our second examining the wider implications of the blackout and its bearing on the pace and priorities of decarbonisation in European power markets.

{kind=link}

Get The Inside Track

Ed Crooks’ Energy Pulse is featured in our weekly newsletter, alongside more news and views from our global energy and natural resources experts. Sign up today via the form at the top of the page to ensure you don’t miss a thing.